A debt-to-income ratio of 40% and an advance payment out of 20% are the thing that extremely finance companies like to see into a home loan app. Might undertake even worse amounts, but costs and APR’s could go up because of this. Including, an advance payment off lower than 20% typically results in necessary mortgage insurance coverage. This advance payment specifications does not submit an application for Government guidance software such as FHA, in which individuals may have installment loans New Jersey a lower life expectancy credit score and you will money but nonetheless found funding.

Regulators Applications

The newest piggyback loan is eliminate the dependence on personal financial insurance of the covering 80% of one’s house’s really worth with the earliest mortgage, since the 2nd financing helps buy a portion of the down payment.

Federal Guidelines Programs

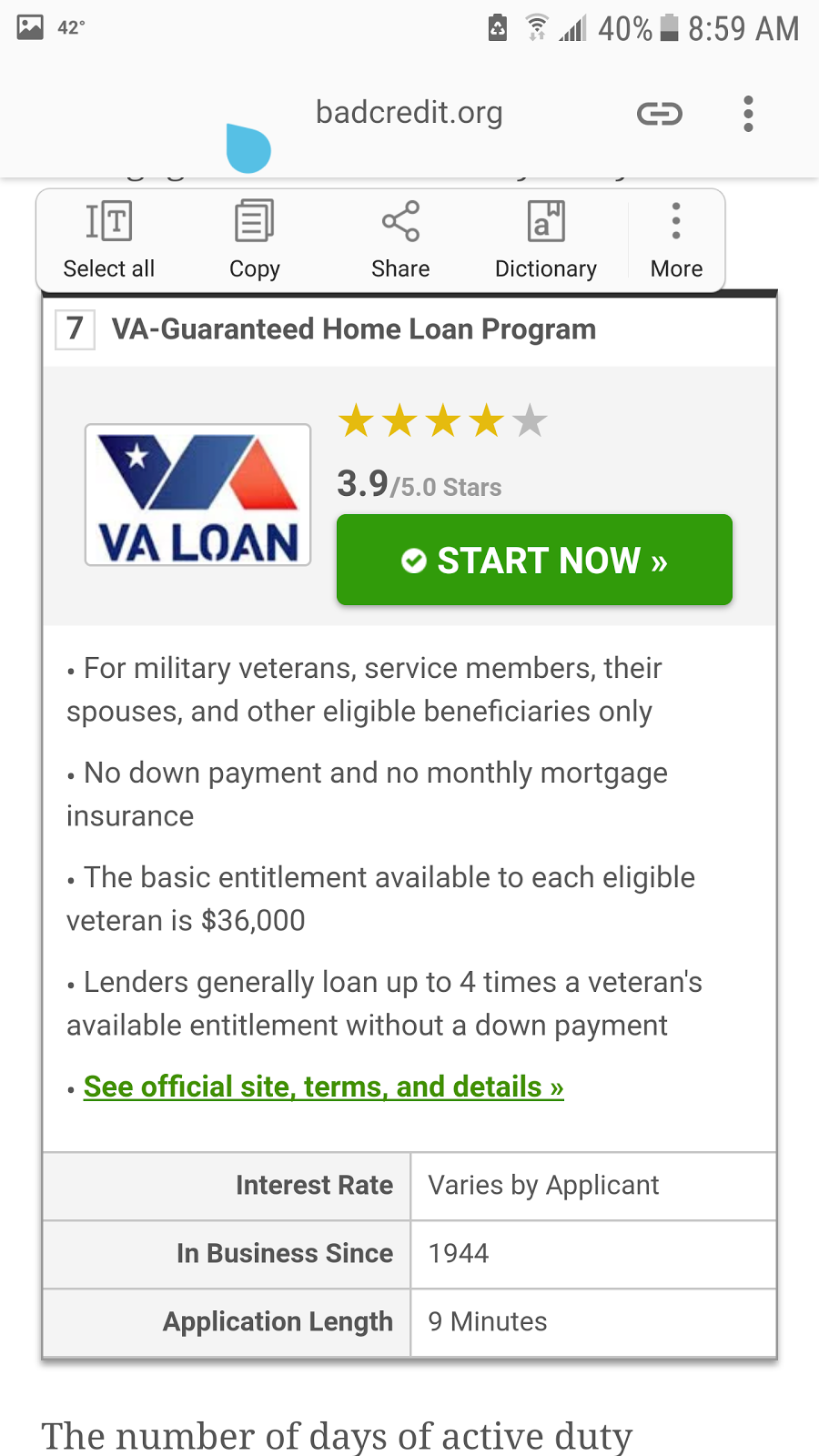

Possible home buyers who don’t find what they’re seeking from the among nation’s personal banking institutions may prefer to take an excellent view a number of the mortgage selection government entities offers. Included in this ‘s the financing system at the Pros Administration, that gives mortgage loans which have no down. At exactly the same time whole lot, Va money do not require private mortgage insurance rates. The new service do, yet not, costs a financing fee, and this differs from 1.2% to 3.3%. Making a volunteer downpayment will reduce that it costs. Just in case you may be wanting to know, yes you actually have as a qualified veteran discover one of them unbeatable marketing.

If you aren’t a veterinarian, you may also take into account the Government Property Administration’s mortgage characteristics. The fresh new FHA has the benefit of loans to people that have a credit history of at least 580 and you may who can set at the least step three.5% down. Government entities service also offers mortgages to own lower credit scores, nevertheless needs more funds off with our funds.

USDA fund might help people with lowest income in rural pieces of condition be eligible for a great subsidized reduced-attention mortgage. Given the lowest society thickness during the all of the condition, very portion qualify.

The LHC Selection Traditional System support individuals which have money constraints lower than $99,000 to track down advance payment advice minimizing interest levels. After you’ve removed the application, you can experience a beneficial pre-approved bank and you can coach services to help you have the restriction guidelines you can.

This choice is not limited to basic-date homeowners, and like where the funds are spent on. You might select downpayment guidelines, closing costs, otherwise prepaid recommendations. The latest eligibility and direction accounts vary from the areas, making it essential that any possible members talk to their regional organizations in advance of it incorporate.

A special program the condition of Louisiana also provides ‘s the Home loan Borrowing Certification program. This method was created to assist people afford their annual property taxation. For the Louisiana, you need to be an initial-big date homebuyer, an experienced, or if you need certainly to get a home for the a certain area become qualified.

For individuals who use and you are acknowledged, you’re going to get a federal tax credit in your yearly taxes you to definitely is equal to 40% of your own yearly financial rates around $2,000 for every tax season. When you have left capital, it will carry-forward around 36 months.

The borrowed funds Revenue Bond system is one that all residents you should never appear to know much about. Choices are readily available for both designers serving lowest-money people and home buyers. This option allows anyone who is approved rating financing having rates of interest that will be beneath the latest having a conventional loan, FHA, or USDA financing.

The home involved should be most of your household, and you’ve got to get to know the cash restrictions you to differ by condition. Simultaneously, your house we wish to pick needs to be underneath the county’s cost maximum, therefore are unable to have possessed property in the past around three age.